Más información sobre el libro

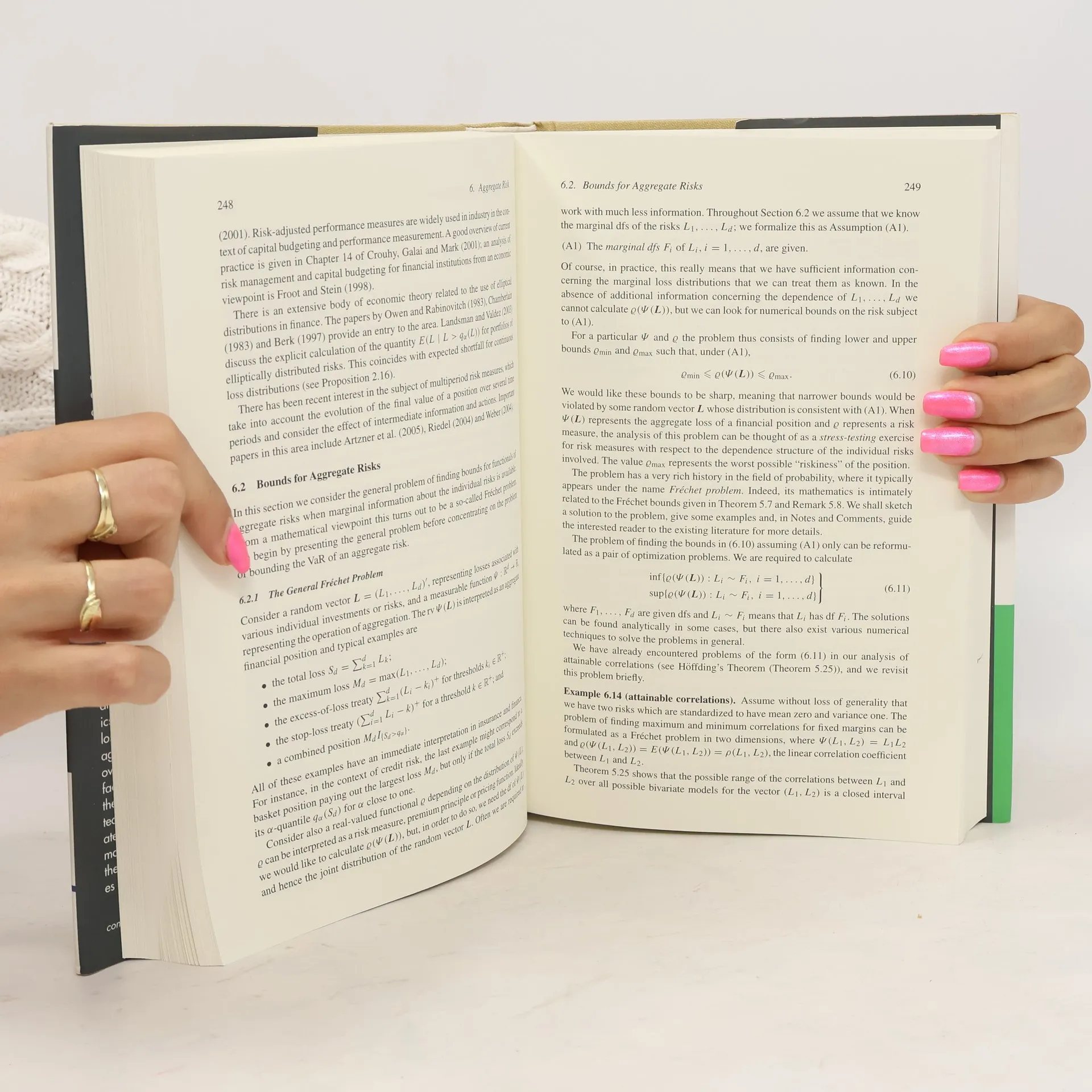

The implementation of sound quantitative risk models is crucial for financial institutions, a trend accelerated by regulatory frameworks like Basel II. This book offers a thorough exploration of theoretical concepts and modelling techniques in quantitative risk management, providing financial risk analysts, actuaries, regulators, and students with practical tools for real-world challenges. It addresses market, credit, and operational risk modelling, formalizing standard industry approaches and presenting recent advancements that rectify existing deficiencies. Drawing from various quantitative disciplines, including mathematical finance, statistics, and actuarial mathematics, the text discusses key concepts such as loss distributions, risk measures, and risk aggregation principles. A central theme is the necessity of addressing extreme outcomes and the interdependence of key risk drivers. Techniques utilized include multivariate statistical analysis, financial time series modelling, copulas, and extreme value theory, with a specialized chapter on credit derivatives. Based on courses for master's students and professionals, this book serves as a unique and essential reference, poised to become a standard in the field.

Compra de libros

Quantitative Risk Management: Concepts, Techniques, Tools, Alexander J McNeil, Rüdiger Fey, Paul Embrechts

- Idioma

- Publicado en

- 2005

- product-detail.submit-box.info.binding

- (Tapa dura)

Métodos de pago

Nos falta tu reseña aquí

- Título

- Quantitative Risk Management: Concepts, Techniques, Tools

- Idioma

- Inglés

- Autores

- Alexander J McNeil, Rüdiger Fey, Paul Embrechts

- Editorial

- Princeton University Press

- Publicado en

- 2005

- Formato

- Tapa dura

- ISBN10

- 0691122555

- ISBN13

- 9780691122557

- Serie

- Etiquetas

- No ficción, Libros de texto, Comercio, Negocios & Gestión, Gestión & Recursos humanos, Finanzas

- Calificación

- 4,45 de 5

- Descripción

- The implementation of sound quantitative risk models is crucial for financial institutions, a trend accelerated by regulatory frameworks like Basel II. This book offers a thorough exploration of theoretical concepts and modelling techniques in quantitative risk management, providing financial risk analysts, actuaries, regulators, and students with practical tools for real-world challenges. It addresses market, credit, and operational risk modelling, formalizing standard industry approaches and presenting recent advancements that rectify existing deficiencies. Drawing from various quantitative disciplines, including mathematical finance, statistics, and actuarial mathematics, the text discusses key concepts such as loss distributions, risk measures, and risk aggregation principles. A central theme is the necessity of addressing extreme outcomes and the interdependence of key risk drivers. Techniques utilized include multivariate statistical analysis, financial time series modelling, copulas, and extreme value theory, with a specialized chapter on credit derivatives. Based on courses for master's students and professionals, this book serves as a unique and essential reference, poised to become a standard in the field.