Parámetros

- 162 páginas

- 6 horas de lectura

Más información sobre el libro

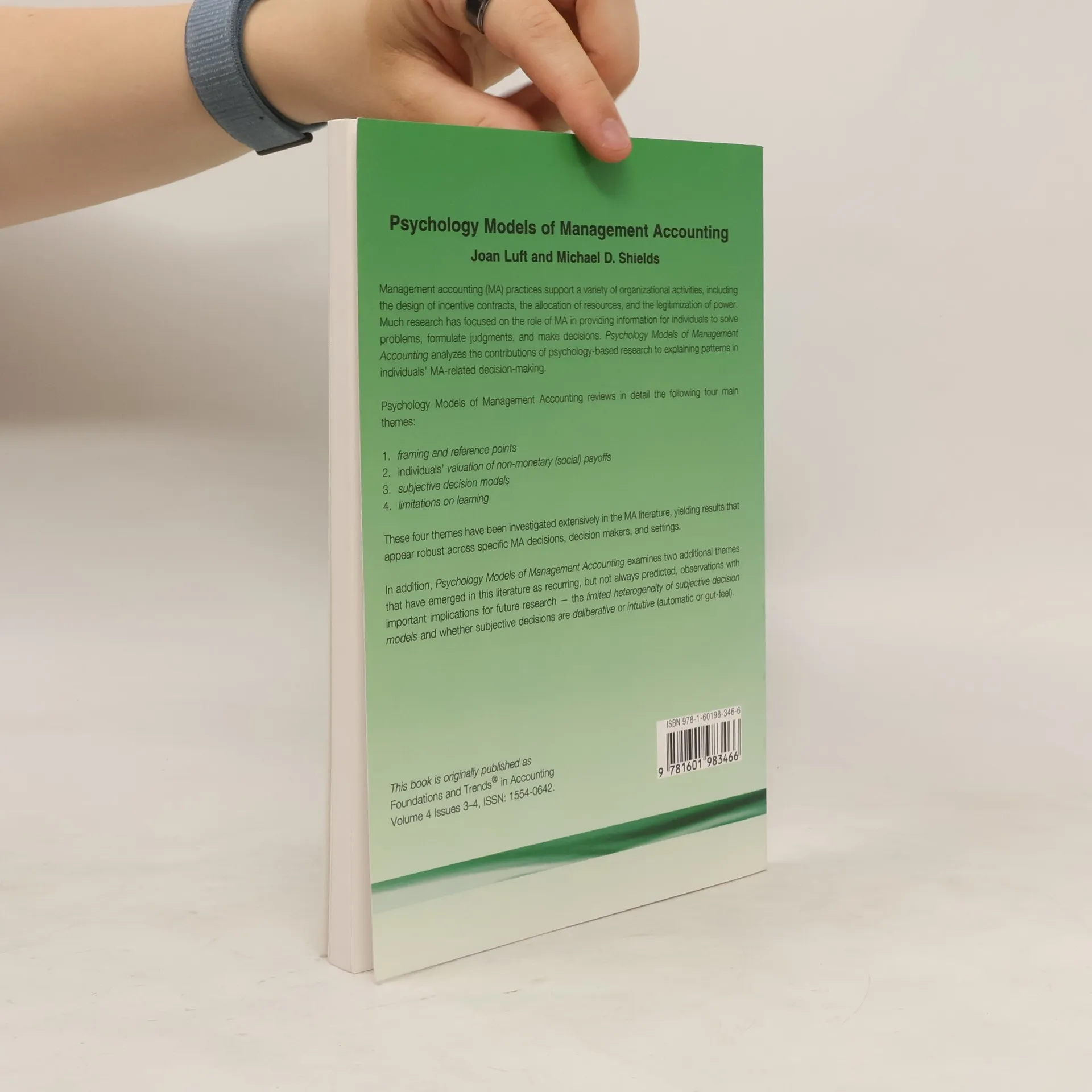

Management accounting (MA) practices support a variety of organizational activities, including the design of incentive contracts, the allocation of resources, and the legitimization of power. Much research has focused on the role of MA in providing information for individuals to solve problems, formulate judgments, and make decisions. Psychology Models of Management Accounting analyzes the contributions of psychology-based research to explaining patterns in individuals' MA-related decision-making. Psychology Models of Management Accounting reviews in detail the following four main 1. framing and reference points 2. individuals' valuation of non-monetary (social) payoffs 3. subjective decision models 4. limitations on learning These four themes have been investigated extensively in the MA literature, yielding results that appear robust across specific MA decisions, decision makers, and settings. In addition, Psychology Models of Management Accounting examines two additional themes that have emerged in this literature as recurring, but not always predicted, observations with important implications for future research - the limited heterogeneity of subjective decision models and whether subjective decisions are deliberative or intuitive (automatic or gut-feel).

Compra de libros

Psychology Models of Management Accounting, Joan Luft, Michael D. Shields

- Idioma

- Publicado en

- 2010

- product-detail.submit-box.info.binding

- (Tapa blanda)

Métodos de pago

Nadie lo ha calificado todavía.

- Título

- Psychology Models of Management Accounting

- Idioma

- Inglés

- Autores

- Joan Luft, Michael D. Shields

- Editorial

- Now Publishers Inc

- Publicado en

- 2010

- Formato

- Tapa blanda

- Páginas

- 162

- ISBN10

- 1601983468

- ISBN13

- 9781601983466

- Serie

- Descripción

- Management accounting (MA) practices support a variety of organizational activities, including the design of incentive contracts, the allocation of resources, and the legitimization of power. Much research has focused on the role of MA in providing information for individuals to solve problems, formulate judgments, and make decisions. Psychology Models of Management Accounting analyzes the contributions of psychology-based research to explaining patterns in individuals' MA-related decision-making. Psychology Models of Management Accounting reviews in detail the following four main 1. framing and reference points 2. individuals' valuation of non-monetary (social) payoffs 3. subjective decision models 4. limitations on learning These four themes have been investigated extensively in the MA literature, yielding results that appear robust across specific MA decisions, decision makers, and settings. In addition, Psychology Models of Management Accounting examines two additional themes that have emerged in this literature as recurring, but not always predicted, observations with important implications for future research - the limited heterogeneity of subjective decision models and whether subjective decisions are deliberative or intuitive (automatic or gut-feel).